Mumbai June 22, 2025 – Hidden Benefits of NPS: For many in India, securing a comfortable retirement remains a top financial priority. While you might consider traditional avenues like mutual funds, a deeper dive into the National Pension System (NPS) truly reveals its compelling hidden benefits of NPS. These significant advantages position NPS as a formidable contender for your retirement savings, particularly when you factor in its unique tax structure and long-term wealth creation capabilities. You are about to discover how NPS can not only outperform some conventional investments but also provide a robust framework for a substantial pension in your golden years.

Try This: NPS Vatsalya Calculator

Think of it like this: You are meticulously planning a grand journey, your retirement. You need the right vehicle – one that is not only reliable but also fuel-efficient and adaptable. For many years, mutual funds were the default choice, like a trusty sedan. But NPS, with its evolving features and inherent strengths, increasingly resembles a sophisticated SUV, ready for diverse terrains and offering unexpected luxuries. Understanding the advantages of NPS becomes crucial for your future.

The Tax Advantage: Why NPS Stands Out for Retirees

The core strength of NPS undeniably lies in its tax efficiency. When you reach retirement, the NPS Tier 1 structure allows you to take 40% of your accumulated corpus as an annuity. The remaining 60%? You can withdraw it as a lump sum, and here’s the game-changer: that lump sum is entirely tax-free. This significant tax saving is one of the key hidden benefits of NPS that truly distinguishes it.

This stands in stark contrast to mutual funds. If you fall into the 30% tax bracket, you face a 10% Long Term Capital Gains (LTCG) tax on the equity portion of your mutual fund withdrawals. This leads to a higher effective blended tax rate, perhaps around 18%, compared to NPS’s significantly lower effective tax outflow. This inherent tax arbitrage hands NPS a considerable edge, putting more money directly into your pocket when you need it most. You are, in essence, enjoying a tax holiday on a substantial portion of your retirement savings, a clear example of the NPS benefits in action.

Can NPS Truly Deliver a Substantial Pension? Let’s Crunch the Numbers!

The question on everyone’s mind: can NPS genuinely provide a “good pension”? Let’s illustrate this with a powerful hypothetical scenario, showcasing more of the hidden benefits of NPS. Imagine you invest ₹50,000 per month in NPS through a Systematic Investment Plan (SIP), increasing your contribution by 10% annually. What does your retirement picture look like after 30 years?

You could see your corpus swell to a remarkable ₹30 crore. From this, you utilize 60% for a Systematic Withdrawal Plan (SWP) – a strategic move that delivers ₹6 lakh per month. Here’s the brilliant part: this withdrawal increases every year, keeping pace with inflation. It’s like having a reliable income stream that constantly adjusts to your rising cost of living, a true breath of fresh air in retirement planning. The remaining 40% (₹12 crore) goes into an annuity, providing an additional ₹5 lakh per month, a stable, fixed income, although this component doesn’t keep up with inflation. This flexibility is another of the profound NPS hidden advantages.

Read More: NPS Vatsalya Tax Benefits Announced: Unlock ₹50,000 Deduction for Your Child’s Future

Combine these, and you are looking at a total monthly pension of ₹11 lakh! Even when you factor in 30 years of inflation at a 6% rate, this equates to a comfortable ₹1.9 lakh in today’s money. “This inflation-indexed withdrawal feature through SWP is a game-changer for long-term retirement planning in India,” remarks Mr. Gupta, a senior financial planner in Mumbai. “It offers a level of financial security against rising living costs that traditional fixed pensions simply cannot match.” You can certainly count this among the crucial advantages of NPS for a secure future.

Let’s visualise that potential retirement income:

| Component of Pension | Amount (After 30 Years) | Monthly Income | Notes |

|---|---|---|---|

| Total Corpus (at 10% CAGR) | ₹30 crore | – | – |

| From SWP (60% of corpus @ 4% withdrawal) | ₹18 crore | ₹6 lakh per month | Withdrawal increases annually with inflation. |

| From Annuity (40% of corpus @ 5% annuity rate) | ₹12 crore | ₹5 lakh per month | Provides a stable, fixed income; does not increase with inflation. |

| Total Monthly Pension | – | ₹11 lakh per month | – |

| Equivalent in Today’s Money (6% inflation) | – | ₹1.9 lakh per month | Maintains your purchasing power against rising costs. |

Hidden Benefits of NPS

Outperforming the Market: NPS Returns in Focus

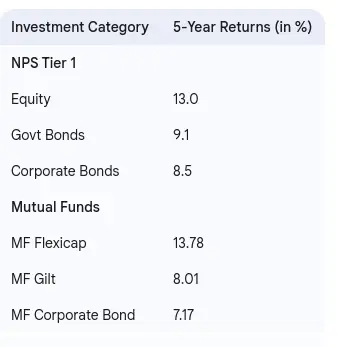

NPS isn’t just about tax benefits; it also delivers competitive returns. Looking at 5-year returns, NPS Tier 1 Equity has clocked in at an impressive 13.0%. Government bonds yield 9.1%, and corporate bonds 8.5%. These strong returns contribute significantly to the hidden benefits of NPS as a retirement vehicle.

Compare this to popular mutual fund categories over the same period: MF Flexicap stands at 13.78%, MF Gilt at 8.01%, and MF Corporate Bond at 7.17%. While a top-performing MF Flexicap might slightly edge out NPS Equity, NPS consistently outperforms mutual funds in the debt categories (Government bonds and Corporate bonds). Why does this matter? Because the overall lower expense ratio of NPS significantly impacts your net returns over extended periods. You’re simply paying less to manage your money, allowing more of your earnings to compound. This makes it a strong choice for long-term wealth creation in India. It’s another compelling facet of the NPS benefits equation.

Here’s a snapshot of recent performance:

Hidden Benefits of NPS

Key Considerations for Your NPS Journey

As you contemplate bringing NPS into your financial portfolio, remember these important points that highlight the multifaceted hidden benefits of NPS:

- Maturity at 60: NPS typically matures when you turn 60, aligning perfectly with most retirement plans.

- Flexibility to Defer: You can defer your NPS corpus withdrawal until age 75. This is incredibly useful if you choose to work longer or simply want your funds to grow further, enhancing the advantages of NPS for flexible planning.

- Extended Entry Age: The upper age of entry into NPS has been raised to 70. This broadens its accessibility, allowing individuals to start contributing later in their careers and still reap the NPS benefits.

- Operational SWP: The Systematic Withdrawal Plan (SWP) feature is now fully operational, offering you a structured, inflation-adjusted withdrawal mechanism to enhance your post-retirement income. This is fantastic news, putting more control in your hands and further cementing the NPS hidden advantages.

In essence, the hidden benefits of NPS are no longer a secret. With its superior tax treatment, robust potential for generating a substantial pension, competitive returns, and increasing flexibility, NPS is emerging as an indispensable tool for securing your financially independent retirement. For anyone diligently planning their golden years in India, a comprehensive evaluation of NPS alongside traditional investment avenues is, in my opinion, more crucial than ever before. You owe it to your future self to explore this powerful option for Indian retirement planning and capitalize on these incredible NPS benefits.